SSR Mining Stock: Ignore The Weak Q1 Results (NASDAQ:SSRM) |

您所在的位置:网站首页 › 行权日是什么时候 › SSR Mining Stock: Ignore The Weak Q1 Results (NASDAQ:SSRM) |

SSR Mining Stock: Ignore The Weak Q1 Results (NASDAQ:SSRM)

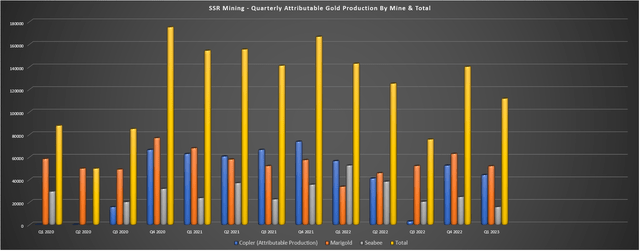

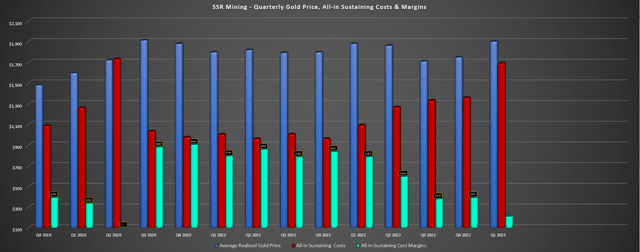

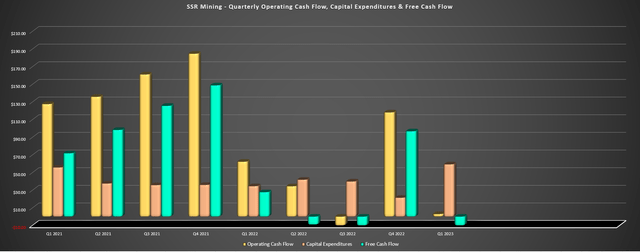

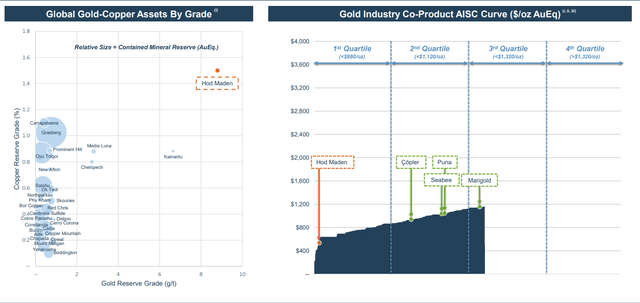

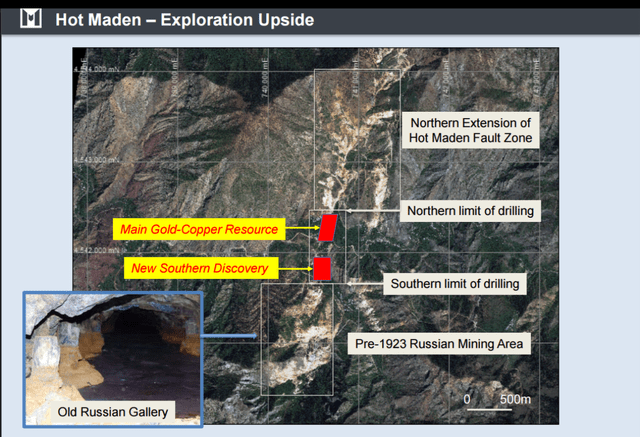

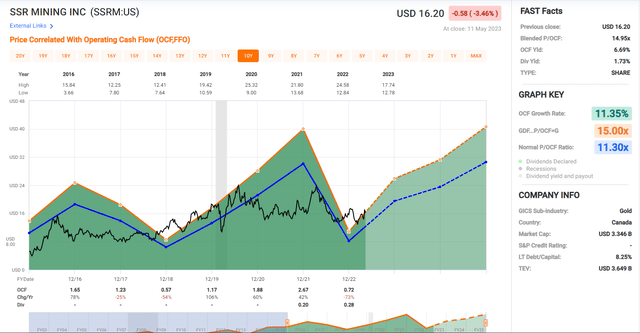

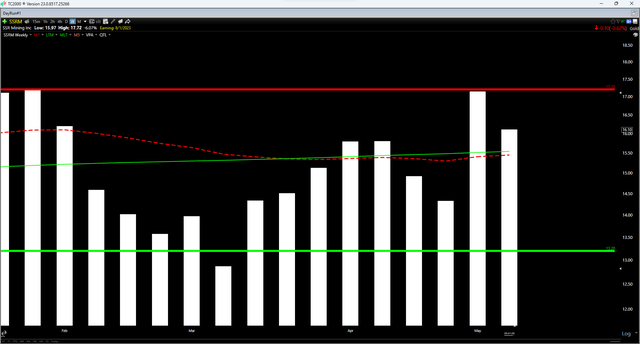

Dazman/E+ via Getty Images We're more than halfway through the Q1 Earnings Season for the Gold Miners Index (GDX) and one of the most recent companies to report its results is SSR Mining (NASDAQ:SSRM). From a headline standpoint, the company's numbers certainly weren't pretty, with ~146,900 gold-equivalent ounces [GEOs] produced at all-in sustaining costs of $1,693/oz and revenue down 11% year-over-year despite stronger metals prices. However, Q1 was an abnormally weak quarter due to much lower production at Seabee and 脟枚pler and sustaining capital being front-end weighted, translating to ugly Q1-23 results. Let's take a closer look at the results below.  SSR Mining Operations - 脟枚pler (Company Website) Q1 Production & SalesSSR Mining released its Q1 results last week, reporting quarterly production of ~146,900 GEOs, a 15% decline from the year-ago period (Q1 2022: ~173,700 GEOs). The sharp decline in output was related to lower sulfide grades at 脟枚pler that was only partially offset by higher oxide grades, and a significant decline in production at Seabee, which saw equipment downtime in Q1 and was up against difficult comps after enjoying grades above 17.0 grams per tonne of gold in Q1 2022. And while Marigold and Puna had better quarters with ~52,000 ounces of gold produced and ~28,400 GEOs produced, respectively, this wasn't able to offset the tough comps at its two higher-margin assets.  SSR Mining - Quarterly Attributable Production by Mine & Total (Company Filings, Author's Chart) Beginning with its flagship asset, 脟枚pler, the asset produced just ~55,100 ounces of gold (100% basis) in the quarter, down over 21% from the ~70,600 ounces of gold produced in the year-ago period. As noted above, while oxide grades were up year-over-year with significantly more tonnes stacked (~188,000 tonnes at 1.22 grams per tonne of gold), sulfide grades were down sharply and the higher throughput of ~724,000 tonnes and slightly higher recoveries still translated to materially lower production year-over-year. The result was that all-in sustaining costs soared to $1,420/oz from $955/oz in the year-ago period, providing little help to what would already be a high-cost quarter.  Marigold Operations (Company Website) Moving over to the much lower-grade Marigold Mine in Nevada, production was up significantly year-over-year to ~52,000 ounces, but this was due to easy year-over-year comps (Q1 2022: ~37,000 ounces produced). The increase in production was driven by higher tonnes stacked and a slightly higher average gold grade, with ~5.37 million tonnes stacked in Q1 at an average grade of 0.42 grams per tonne gold. SSR Mining noted in its prepared remarks it expects to recover the remainder of the material stacked last year with a slower turnaround in Q2, and also confirmed that it's stacked more competent ore this year with investors able to expect more normal leach cycles, which should translate to more predictability in terms of ounces recovered. Unfortunately, the significant increase in production did not translate to lower unit costs, with Marigold's AISC increasing nearly 6% year-over-year to $1,663/oz. However, it's important to note that cash costs were relatively flat at $1,066/oz and the increase in AISC was related to significant sustaining capital in the period related to haul truck purchases, with Q1 sustaining capital of ~$29.0 million coming in at ~36% of the annual guidance range. Hence, there's no reason to believe that Marigold can't meet its cost guidance of $1,315/oz to $1,365/oz despite the slow start to 2023, and while cyanide costs continue to be pressured, the company is getting some help from lower fuel prices and a weaker United States Dollar.  Seabee Mine - Saskatchewan (Google Earth) Finally, looking at SSR Mining's smallest gold operation, Seabee, the mine produced just ~15,800 ounces in Q1 2023, a significant decline from ~52,600 ounces in Q1 2022. While this is an alarming drop on a year-over-year basis, Seabee had to lap an unusually strong quarter where it benefited from head grades of 17.7 grams per tonne of gold. And the mine unfortunately saw equipment downtime in Q1 that shifted the mining sequence, making for a far worse quarter than planned. That said, SSR Mining expects Seabee's grades to improve materially as the year progresses, with AISC set to improve from the $2,207/oz reported in Q1 with lower sustaining capital and higher volumes. Costs & MarginsMoving over to costs and margins, SSR Mining's consolidated AISC came in at $1,639/oz in Q1, a 55% increase from year-ago levels. The higher costs were related to fewer ounces sold and a significant increase in sustaining capital, which soared from $38.7 million to $51.7 million, placing a dent in margins in the period. In fact, despite a higher average realized gold price of $1,902/oz, AISC margins plunged to $206/oz in the quarter, a 73% decline from Q1 2022. That said, investors can ignore these abnormally bad Q1 results and I would expect a significant improvement in margins in Q2 and H2 2023, with sustaining capital spending for the year being lumpy in Q1 and production being back-end weighted which will benefit unit costs.  SSR Mining - Quarterly AISC, Gold Price & AISC Margins (Company Filings, Author's Chart) That said, the weaker margins and lower gold sales certainly didn't help from a financial standpoint, with SSR Mining reporting revenue that was down sharply to just $314.6 million (Q1 2022: $355.5 million), and operating cash flow of $3.0 million vs. $62.2 million in the year-ago period. The result was a cash outflow of $56.3 million in the period vs. positive free cash flow of $27.7 million in Q1 2022, with SSR Mining ending the quarter with ~$300 million in net cash and ~$560 million in cash and cash equivalents. The good news is that we will see a return to positive free cash flow in the back half of the year and while Q1 was ugly, SSR Mining continues to have one of the stronger balance sheets sector-wide.  SSR Mining - Quarterly Operating Cash Flow, Capex & Free Cash Flow (Company Filings, Author's Chart) Operating cash flow was $90.9 million in Q1 2023 vs. $130.8 million in Q1 2022 when adjusting for unfavorable changes in unfavorable working capital movements. Recent DevelopmentsAs for recent developments, I've typically focused on exploration success for the company and its continued strategy of building on land packages around existing assets, including its Taiga Gold acquisition, increased ownership in at 脟枚pler with its consolidation of Karaltepe, and work to build on reserves at Marigold with targets south of Marigold (New Millennium, Trenton Canyon, Buffalo Valley). However, we saw a significant development at quarter-end in Turkiye, with SSR Mining finally putting some of its cash hoard to work to scoop up an initial 10% interest in the high-margin Hod Maden Project in Turkiye. For those unfamiliar, Hod Maden was previously shared by Horizon Copper and Lidya Madencilik, SSR Mining's (and previously Alacer) partner for the past decade at its 脟枚pler Mine in Turkiye. The recent deal will make SSR Mining the operator at the Hod Maden gold-copper project, with an initial $150 million payment for a 10% interest followed by structured milestone payments to earn another 30% for $150 million, with a requirement to pay $84 million to Lidya if it is successful in adding an additional 500,000 GEOs of mineral reserves above the current reserve base. This would translate to a total payment of $354 million for its 40% interest (before capital spent on early works and construction), an attractive price to pay to secure a 40% interest in one of the highest-grade assets globally in a jurisdiction where it already operates.  Hod Maden Co-Product AISC Curve & Global Gold Assets by Copper Grade (Company Presentation) The Hod Maden Project is an intermediate-sulfidation epithermal deposit with gold and copper mineralization and the plan is to mine the asset from underground over a 13-year mine life. The project lies east of the high-grade Murgul copper mine in Artvin Province, Turkiye, with a large land package of ~3,500 hectares that hasn't got the attention it deserves from an exploration standpoint since it was acquired from Mariana. As the chart above shows, this is an asset that has industry-leading copper grades (~3.0 million ounces of gold in all categories and ~351 million pounds of copper at an M&I grade of 10.6 grams per tonne of gold and 1.8% copper), and co-product AISC expected to come in below $600/oz per the 2021 Feasibility Study.  Hod Maden Exploration Upside (Mariana Resources) Looking at the above map provided by Mariana, we can see that the Main Zone which is the focus of the current mine plan makes up just a fraction of the total land package, with a Southern Discovery made by Mariana less than 500 meters away, previous mine workings further to the south, and SSR Mining has noted that there could be upside east of the Main Zone with zinc mineralization on a separate structure. So, this is ultimately an asset that could see a meaningful mine life extension, and with past drill results like 69.6 meters at 62.7 grams per tonne of gold and 2.60% copper in drill hole HTD-71, this is arguably a top-3 asset in the sector from a grade standpoint, which should excite SSR Mining investors that will control a majority interest in this asset. Even if we include the impact of inflationary pressures and assume a 20% increase in upfront capex ($309 million to $371 million) and a 15% increase in operating costs to ~$700/oz, SSR Mining will only require modest capex for its share of construction (~$160 million), and this asset will be a ~80,000 ounce producer on a gold-equivalent basis (first five years) with sub $700/oz costs. As shown in the chart above, this would positively impact SSR Mining's margin profile, with its current AISC margins closer to $1,300/oz when adjusting for the elevated sustaining capital this year. To summarize, I see this as a brilliant move by the company, and while some other development assets made sense to tuck into the portfolio with lots of developers on the sale rack, this is a great and logical fit for SSR Mining at the right price with very modest capex, allowing it to continue with its attractive capital returns to shareholders (buybacks and dividends). Valuation & Technical PictureBased on ~207 million shares outstanding and a share price of US$16.30, SSR Mining trades at a market cap of $3.37 billion and an enterprise value of ~$3.07 billion. This leaves the company trading at a slight discount to its estimated net asset value of ~$3.90 billion when including its future 40% interest in Hod Maden ($400 million on an estimated $1.0 billion NPV (5%). This is a very reasonable valuation given the company's continued exploration success that points to potential reserve growth at 脟枚pler, plus a slight premium for its silver exposure from the company's Puna Mine that's in Argentina.  SSR Mining - Historical Cash Flow Multiple (FASTGraphs.com) Meanwhile, from a cash flow standpoint, SSR Mining trades at ~7.8x FY2023 cash flow per estimates based on current estimates of $2.07. This is a discount to its historical cash flow multiple of 11.3, but a slight premium to some of its intermediate producer peers like Eldorado Gold (EGO) and Evolution Mining (OTCPK:CAHPF), and even some larger producers like Barrick Gold (GOLD). Using what I believe to be a more conservative multiple of 10.0x cash flow to reflect its new ownership of a high-margin asset in Turkiye and its silver exposure, I see a fair value for SSR Mining of US$20.70.  SSR Mining - 6-Month Chart (TC2000.com) However, while this fair value estimate points to a 26% upside from current levels, I require a minimum 35% discount to fair value to justify starting new positions in mid-cap producers. After applying this discount, SSR Mining's ideal buy zone to ensure an adequate margin of safety would come in at US$13.50 or lower, suggesting that the stock is not in a low-risk buy zone currently. This doesn't mean that the stock can't go higher, and the recent Hod Maden deal is certainly transformational. However, with no strong support until US$13.20 and SSRM in the upper portion of its short-term support/resistance range, I remain neutral on the stock for now and see more attractive opportunities elsewhere. SummarySSR Mining's Q1 results were certainly softer than most of its peers, with industry-lagging AISC margins and just ~112,000 attributable ounces of gold produced, its weakest quarter since the Alacer Gold deal excluding the temporary shutdown in Q3 2022. The good news is that with production being back-end weighted and sustaining capital being front-end weighted, we should see much better quarterly results as the year progresses, especially if the gold price can continue to hang out above $1,950/oz. That said, I prefer to only buy miners when they're out of favor and trading at deep discounts to fair value. And while I see the Hod Maden as an upgrade to the investment thesis, I see better reward/risk bets elsewhere in the sector for now. |

【本文地址】